Understanding the Taxation of Selling Your UK Company: Comparing BADR and SSE

For business owners in the UK, understanding how the sale of your company will be taxed is essential to protect your wealth and make the most of available reliefs. In this article, we’ll explore the tax implications of selling a UK company when you personally own the shares and claim Business Asset Disposal Relief (BADR), as well as when the company is owned within a group structure and qualifies for the Substantial Shareholdings Exemption (SSE). We’ll also highlight the differences in tax rates and provide an example calculation.

Business Asset Disposal Relief (BADR)

What is BADR?

Business Asset Disposal Relief (formerly known as Entrepreneurs’ Relief) reduces the rate of Capital Gains Tax (CGT) on qualifying disposals of business assets, including shares in a trading company.

Key conditions for BADR:

- You must be an individual, not a company.

- You must have owned at least 5% of the shares and voting rights in the company.

- You have not utilised your £1 million lifetime limit of BADR

- You must have been an officer or employee of the company (or of a company in the same group).

- The company must be a trading company (or the holding company of a trading group).

- These conditions must be met for at least two years before the date of disposal.

BADR Tax Rates:

- 14% for disposals in the 2025/26 tax year

- 18% for disposals in the 2026/27 tax year and onwards

Substantial Shareholdings Exemption (SSE)

What is SSE?

The Substantial Shareholdings Exemption is available to companies (not individuals) disposing of shares in trading subsidiaries. If the disposal qualifies, it allows the gain to be completely exempt from corporation tax.

Key conditions for SSE:

- The disposing company must have held at least 10% of the ordinary share capital of the subsidiary for at least 12 months in the last six years before disposal.

- The subsidiary must be a trading company or the holding company of a trading group.

- The disposing company itself must also be a trading company (or a member of a trading group).

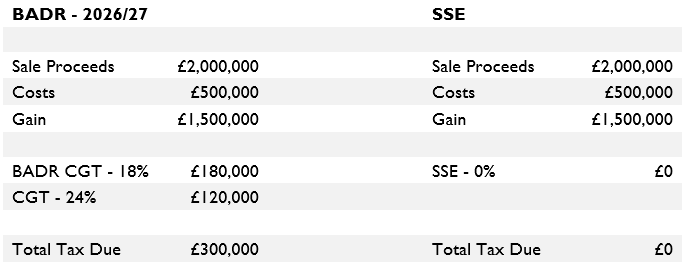

Example Calculation

What Happens After Claiming SSE?

After claiming SSE, while the gain is exempt from corporation tax, the sale proceeds remain within the company. This creates a new set of planning considerations:

Funds Remain in the Company:

Since the proceeds are within the company, they are not immediately available for personal use. If the owners want to extract the cash, this will typically trigger additional tax charges, such as income tax on dividends or income tax/national insurance on bonuses or salary.

Tax-Efficient Extraction Options:

The owners can consider extracting funds over time using a combination of:

- Dividends: Typically taxed at the dividend rates (8.75%/33.75%/39.35%) on the individual.

- Directors’ loans: Repayment of loans can be tax-free, but new loans to directors may have tax implications if not repaid.

- Pension contributions: Up to annual and lifetime limits, which can be a very tax-efficient method.

Reinvestment in the Company:

Alternatively, the company can reinvest the proceeds in further business activities, such as:

- Purchasing commercial or residential property (subject to corporation tax rules and property taxes like SDLT).

- Expanding trading activities or acquiring new subsidiaries.

- Investment in qualifying assets to generate future profits within the company structure.

Key Takeaways

- BADR is designed for individual shareholders and provides a reduced CGT rate on the sale of qualifying shares.

- SSE is only available for companies disposing of shares in trading subsidiaries and provides a full exemption from corporation tax.

- While SSE eliminates corporation tax on the disposal, extracting the funds for personal use can still trigger tax charges that must be managed carefully.

- Thoughtful planning is essential, whether you intend to extract funds tax-efficiently or reinvest in the company’s future growth.

Final Thoughts

Both BADR and SSE offer valuable reliefs, but they apply in different scenarios and have very different practical implications for your wealth. Speak to one of our expert tax advisers at Dragon Argent for a confidential consultation and discover how we can help you protect and grow your assets.